Bookkeeping Fundamentals

Cash vs Accrual Accounting in Canada: What to Use and When

May 25, 2026

You sent an invoice in November. The cheque arrived in February. Your bookkeeping software put the revenue in February. Your accountant moved it to November at year-end. One of those treatments is right for tax purposes; the other is right for managing cash — and the gap between them is what cash vs accrual accounting in Canada is about.

This post explains which method Canadian businesses are actually allowed to use under the Income Tax Act, what each method tells you about the business, and the four moments a growing business outgrows the cash method even when it's still allowed for internal bookkeeping.

Key takeaways

The Income Tax Act allows the cash method only for farming and fishing businesses (section 28(1)). Every other Canadian business — sole proprietors, corporations, professionals, e-commerce, agencies — must compute taxable income on the accrual method.

Cash accounting records revenue when money arrives and expenses when money leaves. Accrual accounting records revenue when it's earned and expenses when they're incurred, regardless of when cash moves.

Many DIY-bookkeeping owners run their books on cash internally and rely on the accountant to convert to accrual at year-end. That works at the smallest scale; it breaks the moment you carry inventory, invoice on net-30 terms, or take prepaid revenue.

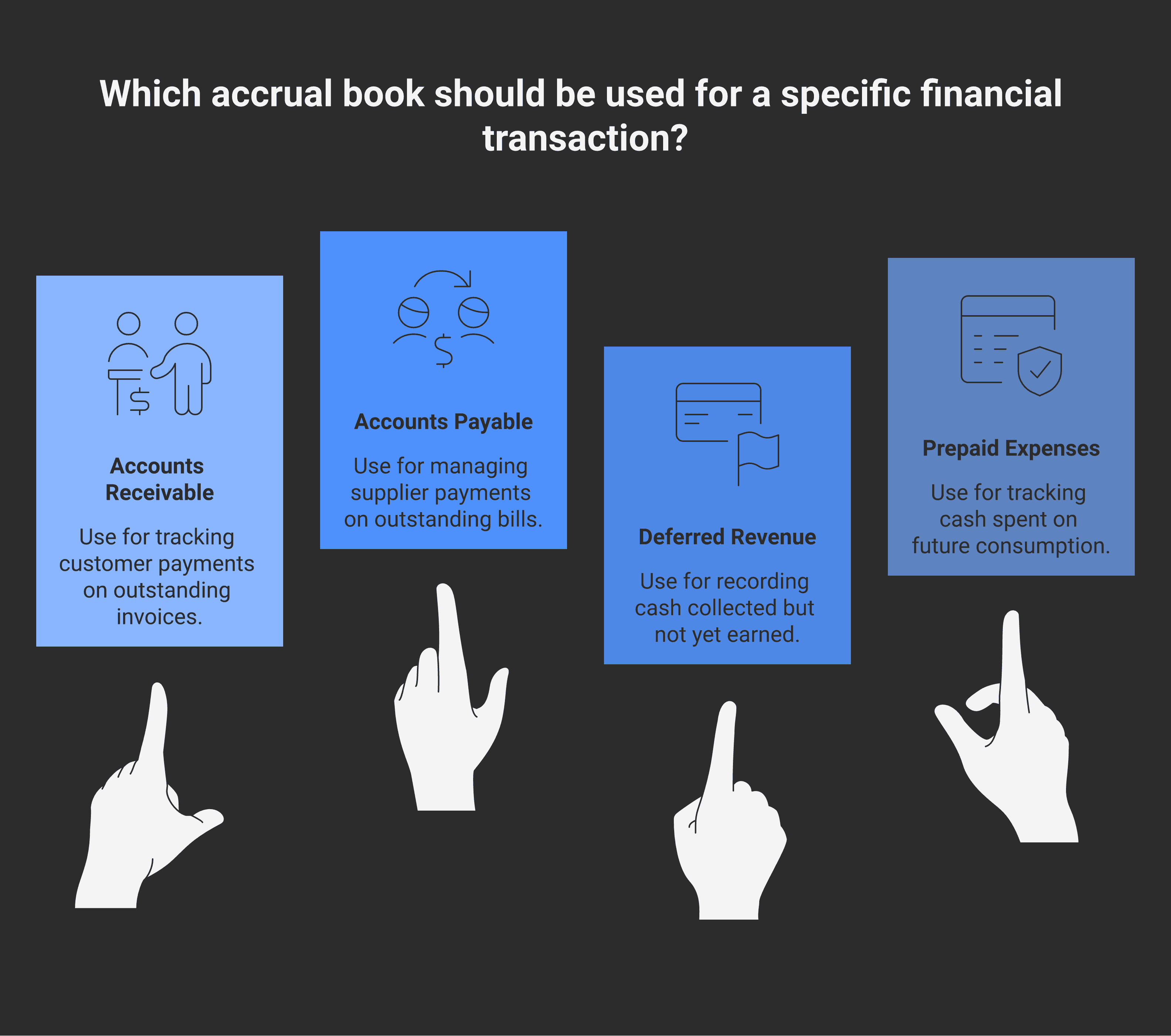

Accrual books use four accounts cash books don't: accounts receivable, accounts payable, deferred revenue, and prepaid expenses. These accounts exist to track the gap between cash and earnings.

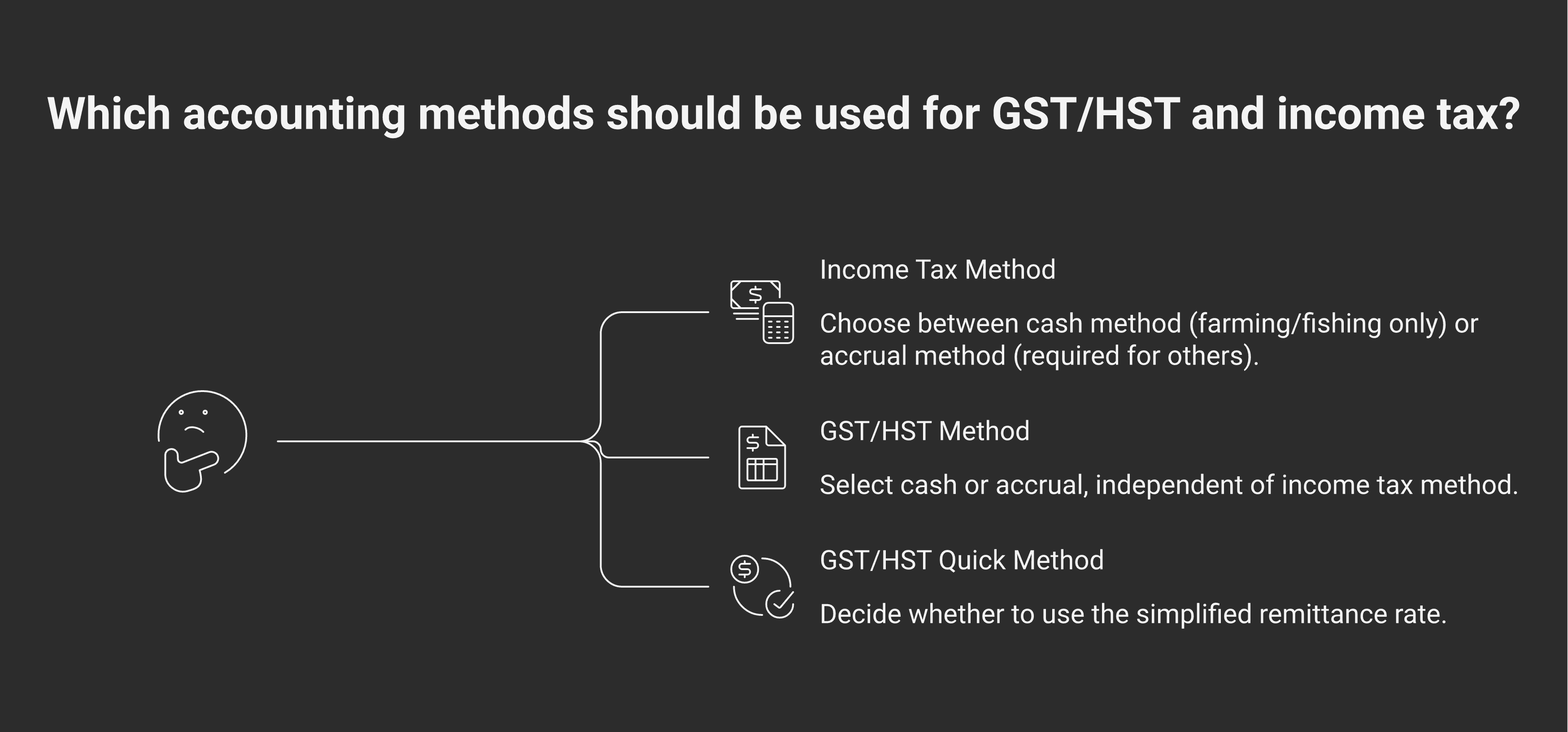

GST/HST has its own separate cash-method election. You can be on accrual for income tax (required for most businesses) and on the GST/HST cash method at the same time. Don't conflate the two rules.

The CRA rule, in one sentence

Under Income Tax Act section 28(1), the cash method is elective and restricted to farming and fishing businesses. Every other Canadian business — sole proprietors filing a T1, corporations filing a T2, professional services, retailers, agencies, contractors — has to compute income on the accrual method under the general profit rule in section 9 of the Act.

That doesn't mean your day-to-day bookkeeping has to be on accrual. It means your tax return does. The bookkeeping reality for many small businesses: keep cash-method books all year, then let the year-end close convert to accrual for the T1 or T2 return.

This works at very small scale. It stops working faster than most owners realize.

What each method actually shows you

Cash accounting answers one question: how much money moved in or out of the business this period.

Accrual accounting answers a different question: how much value did the business create this period, regardless of whether the cash has cleared.

Both answers are useful. They are different answers.

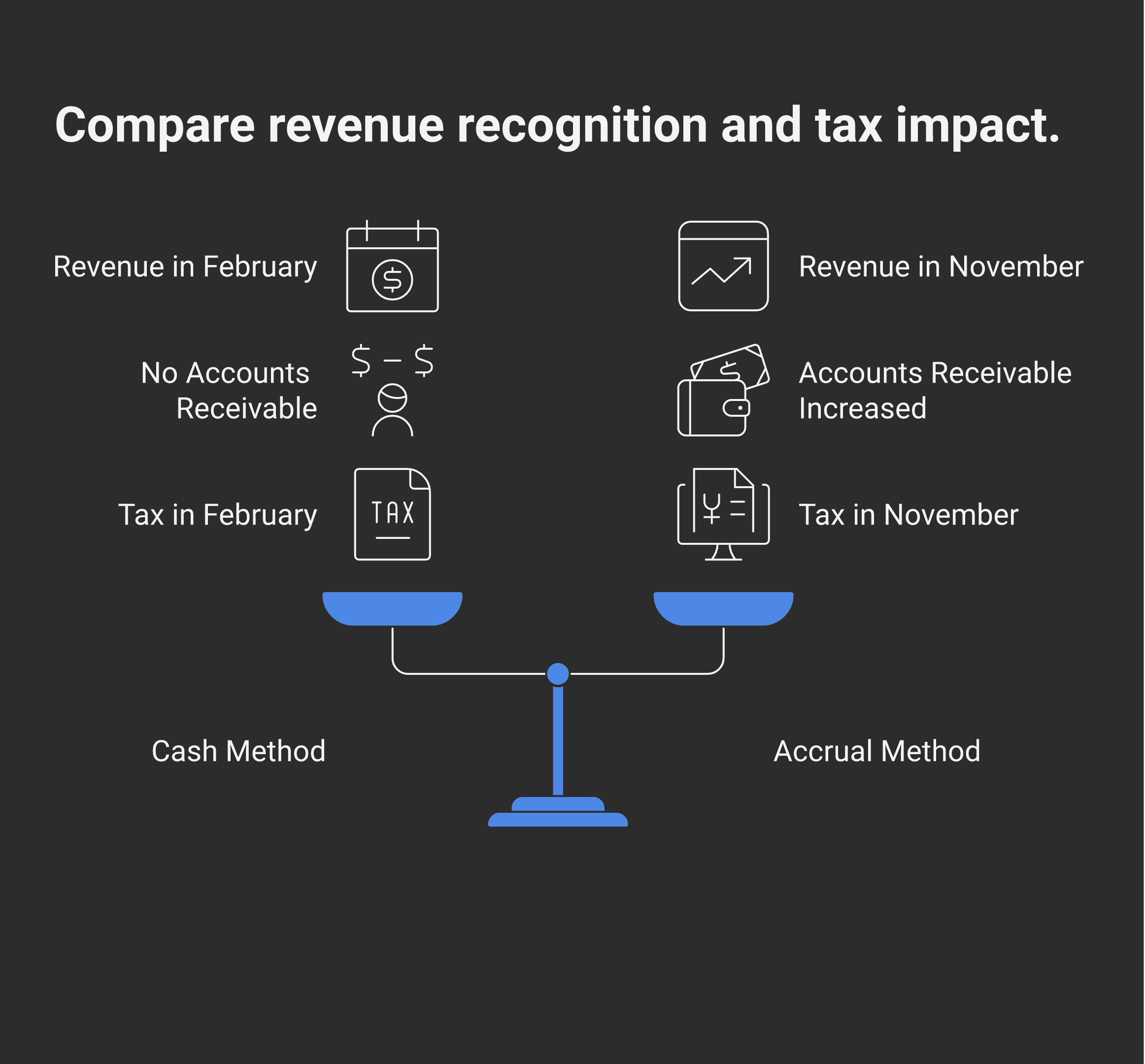

A real example. You spend two weeks in November delivering a project. You invoice on November 30. The client pays on February 10. The accrual answer says: November was a strong month — you earned the revenue then. The cash answer says: November was empty and February had a spike. The work happened in November. The cash arrived in February.

If you're trying to understand your business — which months were profitable, what your margin actually is, whether you can afford to hire — accrual is the right answer. If you're trying to understand whether you can write a cheque next week, cash is the right answer.

A well-run set of books gives you both: accrual books as the operating reality, a separate cash position report on top.

Why owners default to cash — and where it breaks

DIY bookkeeping software (QuickBooks Online, Wave, Xero set to cash) defaults to recording transactions when bank or credit card activity hits the feed. That's cash accounting. It's easy. You can hand-categorize a year of bank transactions in a weekend and call it a year of books.

This works for the smallest businesses with no inventory, no invoicing on terms, no prepaid contracts. Once any of those exist, cash starts giving you a distorted picture.

Specifically:

No accounts receivable. Cash-method books don't show what's owed to you. You can't see your collection cycle, your aging, or how much revenue is sitting in someone else's accounts payable.

No accounts payable. Cash-method books don't show what you owe suppliers. Balances are invisible until they leave the bank.

No matching principle. Revenue and expenses can land in different months even when they relate to the same project. You can't measure project margin or month-over-month profitability.

No inventory tracking. Cash treats inventory purchases as immediate expenses. Accrual recognizes them as assets until sold. The difference is "we lost $40,000 in March" vs "we bought $40,000 of inventory in March."

No deferred revenue. A customer paid you in advance for a year of service. Cash treats the whole payment as January revenue. Accrual spreads it across the twelve months you actually earn it.

The accountant fixes all of this at year-end with adjusting journal entries. The CRA sees clean accrual numbers on the return. But for eleven months of the year, the owner has been looking at the wrong numbers.

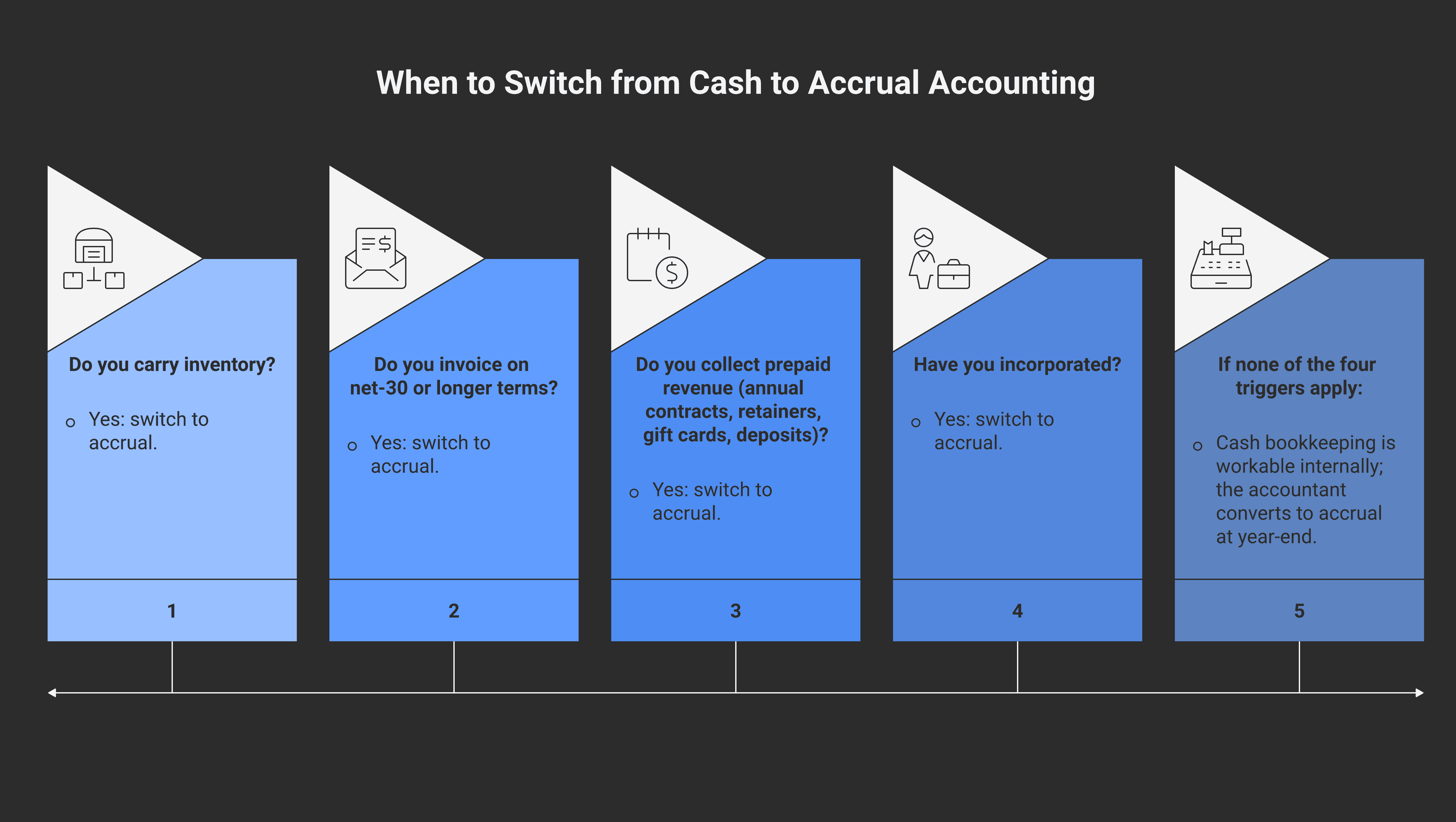

The four moments to switch

Most growing businesses stay on cash internally — with accountant adjustments at year-end — until one of four moments arrives.

You start holding inventory. Selling physical goods means tracking cost of goods sold and inventory value. Cash accounting can't do this in any useful way. Switch to accrual when you place your first wholesale order.

You start invoicing on terms. If your invoices get paid 30, 60, or 90 days later, you need accounts receivable to see your collection cycle. Cash books make a 60-day collection cycle invisible until the cash gap nearly bankrupts you.

You start collecting prepaid revenue. Annual contracts, retainers, gift cards, deposits — anything paid before earned — needs deferred revenue tracking. Cash books overstate revenue in the month of payment and understate every month after.

You incorporate. Corporations file financial statements on accrual whether the internal books were or not. They're also more likely to pay corporate tax instalments and to be eligible for the small business deduction, both of which assume accrual reporting. Running accrual internally from day one of incorporation saves the year-end close from being a multi-week reconciliation.

Most growing businesses hit at least one of these in their first three years. Many hit two simultaneously.

The bookkeeping mechanics

Accrual books have four accounts that cash books don't:

Accounts receivable (asset) — what customers owe you on outstanding invoices

Accounts payable (liability) — what you owe suppliers on outstanding bills

Deferred revenue (liability) — cash you've collected but haven't yet earned

Prepaid expenses (asset) — cash you've spent on something you'll consume over time (annual insurance, prepaid software, prepaid rent)

These four accounts are what accrual is. Setting up accrual books for the first time means opening these accounts in your chart of accounts and recording invoices and bills against them — not against the bank account directly.

The day-to-day workflow is:

Invoice issued → record revenue and AR (no cash movement yet)

Invoice paid → record cash in, AR down (no revenue impact — already recognized when invoiced)

Bill received → record expense and AP (no cash movement yet)

Bill paid → record cash out, AP down

The bank feed still posts the same transactions; the bookkeeper matches them to existing AR/AP entries rather than creating new revenue or expense lines at the moment of payment. The bookkeeping habit shifts from "the bank feed is the source of truth" to "the invoice or bill is the source of truth, and the bank feed confirms when cash has cleared." That shift is the heart of what changes when you go to accrual — and it's well-covered in Modern Axis's bookkeeping basics piece for the broader context.

GST/HST cash method is a different question

The Excise Tax Act has its own cash method for GST/HST that you can elect separately. It is not the same rule as the income-tax accrual requirement. A business can be on accrual for income tax (required if you're not farming or fishing) and on cash method for GST/HST (optional, available to most small businesses under $1.5 million in taxable supplies).

The GST/HST cash method lets you remit sales tax when you actually collect it from the customer, not when you invoice. That helps cash flow on long-payment-cycle work — you're not remitting GST on an invoice that hasn't been paid yet.

There's also the GST/HST Quick Method, which is a different election again — a simplified rate of remittance, not a cash-vs-accrual question. Don't confuse the three rules. A typical small business is on accrual for income tax, possibly on cash for GST/HST, and possibly on the Quick Method for GST/HST remittance calculation. All three settings are independent.

Switching methods

If you've been running cash-method books and you're about to cross one of the four thresholds above, the switch is mechanical:

Identify your accounts receivable balance as of the switch date — invoices issued and not yet paid.

Identify your accounts payable balance as of the switch date — bills received and not yet paid.

Book the opening AR and AP balances as journal entries on the switch date.

From that point forward, record invoices and bills to AR/AP rather than to revenue and expense lines.

Run a parallel cash position report so you still see your bank balance for cash-management decisions.

This is a half-day of work for a typical small business when done early. The cleanup gets dramatically harder the longer you wait. Two years of cash-method books with $200,000 of unrecorded AR and AP is a multi-thousand-dollar catch-up project; the same switch made in month one is a single journal entry.

When the switch lands on a bookkeeper

Modern Books sets up accrual books from day one of every client engagement, including the AR, AP, deferred revenue, and prepaid expense accounts that make a future switch from DIY cash bookkeeping invisible. If you've been on cash books long enough that the year-end close has become a multi-week scramble, the right answer is usually to bring the accrual conversion forward, not to wait for next December. The Modern Books Starter and Mid tiers cover this; book a session if you want to see what the conversion looks like for your specific business.

Frequently asked questions

Is cash accounting legal in Canada for a small business?

For internal bookkeeping, yes. For your tax return, only if you're a farming or fishing business under Income Tax Act section 28(1). Every other Canadian business — sole proprietors, corporations, professional services, retailers — must compute taxable income on the accrual method. Many small businesses run cash books day-to-day and let the accountant convert to accrual at year-end for the T1 or T2 filing.

What's the difference between cash and accrual accounting in plain English?

Cash accounting records revenue when money arrives and expenses when money leaves. Accrual accounting records revenue when you earn it (typically when you invoice the customer) and expenses when you incur them (typically when you receive the supplier bill), regardless of when cash moves. Accrual gives a more accurate picture of how the business is performing. Cash gives a more accurate picture of how the bank account is doing.

Do I have to be on accrual for GST/HST?

No. The GST/HST cash method is a separate election (Excise Tax Act, not Income Tax Act) and is available to most small businesses under $1.5 million in taxable supplies. You can be on accrual for income tax — required for non-farming/fishing businesses — and on cash method for GST/HST simultaneously. Don't confuse this with the GST/HST Quick Method, which is a third option about how you calculate the remittance amount, not when you remit.

When should I switch from cash to accrual?

When you start carrying inventory, invoicing on net-30 (or longer) terms, collecting prepaid revenue, or incorporate the business. Most growing small businesses hit at least one of these triggers in the first three years. Switching is mechanically simple if done early and progressively harder the longer you wait — two years of cash-method books with significant unrecorded AR and AP can become a multi-thousand-dollar catch-up project.

Can my accountant just keep adjusting my cash books at year-end forever?

For very small businesses with no inventory, no terms-based invoicing, and no prepaid revenue, yes. As soon as any of those exist, the year-end adjustment becomes a several-week reconciliation rather than a few hours of journal entries, and the cost compounds with every year you delay the conversion. The accrual books also give you eleven months of usable financial information that cash books don't.

Does QuickBooks Online support accrual?

Yes. QuickBooks Online, Xero, and Wave all support accrual, but they default to cash for new businesses and require setup of AR, AP, and deferred-revenue accounts in your chart of accounts. The day-to-day bookkeeping habit also shifts — you record invoices and bills to AR/AP rather than waiting for the bank feed to recognize the transaction. A bookkeeper can flip the switch in a single session if the underlying books are clean. More posts on bookkeeping software workflows are coming to the Modern Books resource hub.

Is accrual harder than cash?

Day-to-day, slightly — there are more accounts and you record invoices and bills before the cash moves. Once the workflow is set up, the additional effort is small. The real benefit: you get usable monthly numbers all year, not just at year-end after the accountant has done several weeks of adjusting entries. Most owners who've worked on accrual books for six months don't go back.

This post covers general bookkeeping practice in Canada and isn't bookkeeping advice for your business. Software defaults, CRA rules, and the right approach for your specific situation depend on facts not covered above. Talk to a bookkeeper or CPA who knows your numbers before relying on anything you've read here.